If you want to change purchasing, you have to inspire your colleagues from the specialist departments. C-items are process cost drivers and behind the supposed objectivity lies a high degree of emotionality. What influence does this have on the development of your own procurement and how can employees be involved in this?

As a supplier, we have an important appointment with one of the leading industrial companies. After arriving in the meeting room and being provided with coffee, the purchasing manager gets straight to the point: “We would like you to show us further savings potential!” In order to enable a “price” reduction, we talk about the three brand strategy. This approach consists of three brands in two different quality levels. The branded product and the quality own brand are positioned at the highest level. The price difference is in the double-digit percentage range for the same quality. In the second level, the second own brand is positioned, which as a private label focuses on price.

The model arrives and we arrange a test between a branded product and a quality own brand. The choice falls on the hand tool: wrenches. The two brands are sent to the specialist department for the test. The result is surprising, the branded product clearly wins the test. Both wrenches are made from the same material and have the same geometry. We were astonished, because from a factual point of view there is no drastic “difference in quality”.

Objectivity meets emotionality

This incident took place at an important key account customer in the Nuremberg metropolitan region. By “we” I am referring to my former employer, the leading tool retailer in Europe. The quality own brand was introduced in 1973 to create an alternative to branded products. The approach is to be able to offer a price advantage by increasing quantities and concentrating on top-selling items while maintaining high quality. Incidentally, the wrench featured in this story can also be found in my logo.

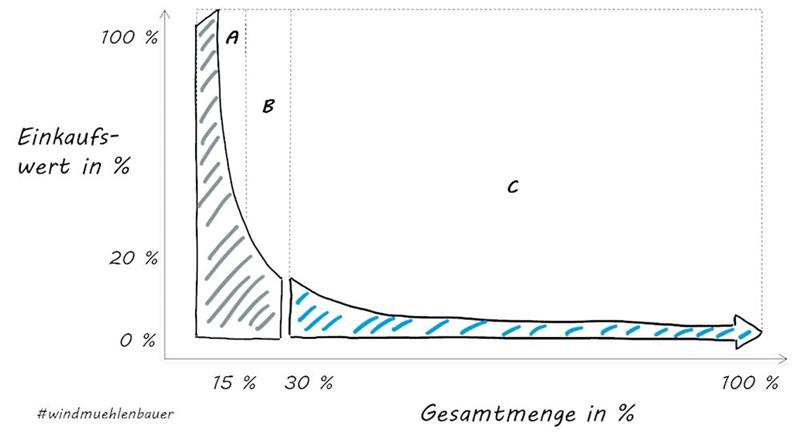

We are talking here about C-articles, which are also often called C-parts. The “C” initially indicates a less important category. From a business perspective, materials and services can be valued according to the ABC analysis. The evaluation is based on the total purchase value and the total quantity. As a rule, this evaluation results in an A-item share of approx. 60-80% of the purchase value and approx. 15-25% of the total quantity of items to be procured. In the case of B items, the share of the purchase value is 10-25% with a quantity share of 30-40%. C-parts are therefore the items that ultimately account for 5-15% of the value, but 40-70% of the total quantity. The following diagram illustrates the ratio described.

C-items are the material group in the company with the highest process costs and therefore consume many hours of employee time. The supposedly simple items such as wrenches, notepads, pens or safety shoes are emotionally charged. The employee (consumer) who uses these items is the real decision-maker in the company because they work with these products on a daily basis. Successful C-parts management can only be implemented if the purchasing department manages to convince and involve these “internal customers”.

High litigation costs for C-articles: Myth or truth?

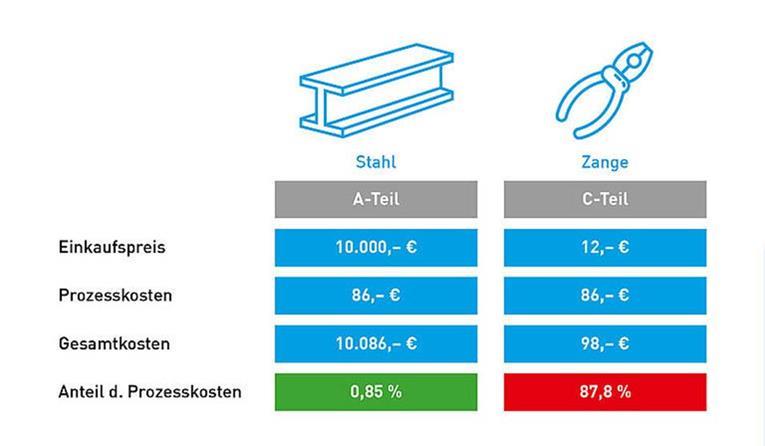

“Process costs are a milkmaid’s calculation” – I have been accused of this before. By process costs, I mean the working time employees spend on an activity, e.g. the ordering process. An order process begins with the employee’s need and ends, in the best case, with the successful booking in the accounting department. According to the study by Mercateo and HTWK Leipzig (Leipzig University of Applied Sciences), these are between €67 and €116 per order. Blumenbecker, an industrial service provider, states process costs of €86. The following graphic illustrates the problem in the key figure “Proportion of process costs”. These costs are significant for several hundreds or thousands of orders. Blumenbecker refers to C-articles as C-parts.

Regardless of whether the process costs are €115, €86 or €50, this shows that employees in the company spend a lot of time ordering “low-value” materials. No added value is created during this time. This is therefore wasted potential. My personal focus is to bring companies and employees into value-adding activities. According to the study mentioned above, high process costs are a reality for many medium-sized companies. But how can these be reduced?

Why the essential user is the real decision-maker!

If you take a closer look, the so-called “essential user” (employee) is the real decision-maker. In order to reduce process costs, they should be actively involved in purchasing. It is therefore important to look at the factors that lead to the acceptance of defined product ranges, suppliers and processes. The situation described at the beginning shows that with C-items, objectivity regularly clashes with emotionality.

Now the objection could be raised that the consumer may only order defined items and therefore emotionality has no influence. This statement can be verified with the maverick buying rate. Maverick buying refers to uncontrolled purchasing by the employee that bypasses the specified procurement process. The term maverick is derived from the cattle breeder Samuel A. Maverick (1803 – 1870), who did not brand his cattle, unlike was customary at the time. The maverick buying rate determined in the study by Mercateo and HTWK Leipzig is between 20-31%. This means that in the end it is the employee who decides where the demand is met. Compliance with the procurement process is therefore not always guaranteed. In many companies, there are ways of ordering items that bypass the purchasing department.

After consultation with the line manager, the requirement can also be submitted via the travel expense report. Or a good contact in financial accounting pays the invoice without insisting on compliance with the procurement process. It is therefore important to maintain communication with specialist departments and requisitioners. If the needs are transparent, successful purchasing processes can be developed. Alham Schmidt, Account Manager at Baseware, also states the same: “A lack of or inadequate communication is probably one of the main triggers for problems (not only) in the professional environment. Who of us hasn’t experienced this? It is therefore essential that the purchasing department talks to the specialist departments, finds out about their needs, discusses the selection of suppliers and makes its own processes and requirements transparent.”

The second test

The purchasing manager understands our arguments and supports a second test. In this case, the wrenches are issued to the specialist department with the logos and identification numbers removed. After the test period, the result surprises us again. The quality own brand performed slightly better than the branded product. This proves the case for the private label. Based on this result, we are working with the purchasing department on approaches to promote the quality own brand. For example, it is included as an alternative product in the electronic catalog to increase awareness. In addition, Strategic Purchasing recommends that the relevant specialist departments concentrate on the quality own brand.

My conclusion

The situation outlined above shows that C-items have a high emotional component. Specialist departments often have a higher level of expertise than the buyer, who usually coordinates and procures many product groups. It is therefore becoming increasingly important for buyers to talk to their “internal customers”. Procurement is all about getting the right product quickly and easily. The fact that employees are used to the usability of providers such as Amazon and the like in their private lives also increases the hurdle. In my view, the success of efficient C-item procurement therefore depends on the ability of the purchasing department to pick up the specialist departments. Process costs and the maverick buying rate can be reduced if the employee can access the desired product quickly and easily.

Leverage potential and reduce maverick buying with Canvas!

A canvas was created in collaboration with Mr. Thomas Auer from UVEX Group Purchasing. Canvas means canvas and is intended to serve as a tool for the next steps. This tool is used for printing and can be filled with Post-it notes.

The canvas contains the following six steps:

- Internal customer

- Understand

- Summarize findings

- Analysis of framework conditions

- Identify quick wins

- Active steps

The first step revolves around the question: “Who are my internal customers or essential users?”. This first step is about identifying the relevant customers in your company. The second step, “Understanding”, is about how you can analyze the problems of internal customers, e.g. with the help of feedback discussions. The lunch table and the relaxed atmosphere can also be used for this purpose. In the back of your mind you can have the thought: “How do I position our purchasing department as a problem solver?”.

From the discussions held, it is important to summarize the findings and determine the greatest need for action. In this step, it is important to keep your internal customers up to date. Communication is crucial for the internal climate. Based on the greatest need for action, analyze the systems, processes and suppliers that are currently available to you. Once you know the needs of your internal customers and the corresponding framework conditions, it’s time for step 5. Define which quick wins you can leverage and now determine the active steps. You can find a few ideas for active steps under point 6.

Peter Prütting is an expert in value-oriented and digital business development. With over 15 years of sales experience from the perspectives of wholesale, manufacturing, and e-marketplaces, he takes a holistic view. His colleagues value him as a customer-centric and focused leader who guides teams through digital transformation. Away from his daily work, he recharges his batteries by mountain biking.

Sources

- Basware A problem and its solution – Maverick Buying https://www.basware.com/de-de/blog/april-2016/maverick-buying-ein-problem-und-seine-loesung

- Blumenbecker C-article management https://www.blumenbecker.com/de/industrie-handel/e-procurement/c-teile-management/

- Contorion C-article https://www.contorion.de/magazin/c-teile-management-in-kmu-viel-potenzial-zur-kostenersparnis

- Hoffmann Group Three Brand Strategy https://www.hoffmann-group.com/DE/de/hom/company/group/history

- Mercateo and HTWK Leipzig study https://www.mercateo.com/corporate/wp-content/uploads/2017/03/Mercateo-Studie_Indirekter-Einkauf-im-Fokus.pdf

- Pixabay Cover picture https://pixabay.com/images/id-1744958/

- Windmuehlenbauer.com Canvas https://my.hidrive.com/lnk/9pgDBosj#file